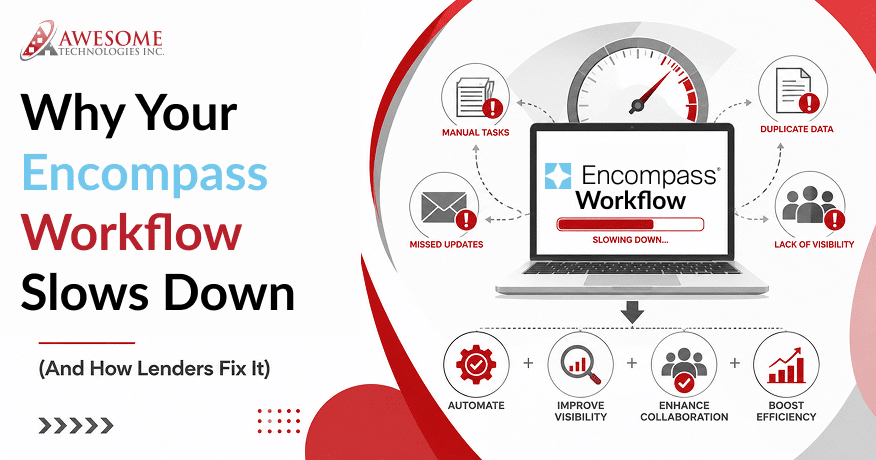

Most of the time a loan processor will not say that loan software is what is keeping them from finishing their job timely. The common phrases you are likely to hear are, “the file kept bouncing back,” “the underwriter requested the same document three times,” or, “we waited a whole week on the borrower’s pay stub.” Encompass® by ICE Mortgage Technology powers the loan manufacturing process for thousands of financial institutions and independent mortgage banks throughout the United States. However, Encompass is often blamed for delays, even though the majority of the delay is because of the workflow created within Encompass.

It is very important to understand this difference because it changes where lenders should find solutions for delays. Encompass provides lenders with tremendous configurability. However, configurability can also create challenges. Loan files from lenders that have never revisited their conditions, document indexing rules, or income calculation logic have built-in delays based on the number of bottlenecks in each loan file and since when this is happening.

This blog will guide operational leaders, production managers, and technology decision-makers working at lenders, who currently operate with the Encompass platform, what causes Encompass workflow bottlenecks? and who are still experiencing delayed cycle times.

If you’re trying to know whether to automate your processes using internal resources, purchase a specialized solution, or implement a fully integrated platform, the following comparison will provide you with a stronger starting point.

What Counts as Encompass Workflow Bottlenecks?

A workflow bottleneck occurs when there is a lag in processing time due to an inactive loan due to a delay by either a person or missing document, or via an interruption caused by an improperly functioning integrated or disconnected system. These circumstances do not consist of a software failure or a technical issue only. Most Encompass workflow problems happen because manual entry of data, dissimilar processing and decision-making by individual operations employees, or having multiple systems that require to re-key data between systems.

The financial burden from ignoring continues to grow quickly. Freddie Mac found that in their 2025 revision to their Cost to Originate Study, the average amount to close a mortgage after the previous quarter’s record low of over $13,400 had reached just under $11,800 in Q2 2025. According to the same study, when Freddie Mac’s Loan Product Advisor offers automated underwriting as well as digital verification, lenders that use those tools pay approximately $1,700 less for each mortgage than lenders who do not use those tools. This gap is not just theoretical. It is the genuine and quantifiable cost relevant to the expense of manual rework within a loan file.

The Tech Architecture Dilemma: Buy vs. Build vs. Partner

In attempting to solve these gaps, tech leaders get three options:

- Build it in-house: A desirable option, but developing custom code or heavy native business rules inside Encompass creates a huge amount of Technical debt. When ICE Mortgage Technology pushes platform updates, your homegrown code breaks down, causing your teams to act as software mechanics.

- Point solutions: Purchasing separate standalone tools for OCR, income, or compliance. Without deep integration, the processor functions as the “human API layer,” continuously switching back-and-forth between tabs and manually copying/pasting data.

Why Encompass Workflows Slow Down in the First Place?

While lenders have different systems and processes in place to originate loans, the following three Encompass workflow problems occur frequently throughout the lending process regardless of the size of the lender’s organization or the number of loans they fund.

- Manual data entry: At this point, many lenders are using Encompass and have no integration between Encompass and any of the other systems they use to process their loans. The processor enters the data from the borrower into Encompass multiple times, as well as into one or more other systems. Each manual entry presents the opportunity for a typo or missing field.

- Inconsistent decision logic: Two underwriters review the same self-employed borrower files and arrive at two separate qualifying income figures. In addition to delaying the loan, both the lender and the borrower are at compliance risk because of inconsistency within the lender’s support of the loan file and creating difficulty when defending the file during an audit.

According to Marina Walsh, MBA’s Vice President of Industry Analysis, the continued elevated origination costs are leading lenders to look for ways to “reduce origination costs and increase productivity.” The answer that she and other industry economists keep referencing is the combination of process improvement and technology as opposed to just adding to headcount.

The Five Biggest Encompass Workflows Bottlenecks

1. Document Indexing and Data Extraction

There may be hundreds of pages in a mortgage file that include pay stubs and bank statements, and tax transcripts, disclosures, verification forms, etc. There would be a person or system that would identify each document type, then extract relevant fields from that document type and enter that data into the correct Encompass fields before any underwriting could start.

| Manual Document Review | Automated Document Extraction |

| Processor identifies the type of document manually | Systems automatically classify uploads with documents |

| Manual data entry by the borrower | Extraction of Structured Data directly into Fields in Encompass |

| More chances of making errors until QC review | Data validation at every stage |

| Can significantly reduce processing time in high-volume scenarios | Minutes of processor time per loan file however it largely depends |

To address this challenge, lenders are using document intelligence solutions built directly into Encompass so as not to require additional time wasted looking at separate web browser tabs to process paperwork.

2. Income Calculation Complexity

Calculating income for underwriting is one of the most complex aspects to assess. It’s not surprising that income remains one of the most conditional parts of the underwriting process. Judgments about self-employment status, commission pay structures, bonuses, and multiple channels of income can all become difficult to understand. Moreover, qualified income is difficult to define by a single calculation file in a spreadsheet.

When three different members of the team calculate qualifying income using three different methods, the loan does not move forward in a smooth manner. It bounces back and forth between the processor, the underwriter, and the loan officer as they all attempt to reconcile their different calculations. This is one of the most clear-cut ways in which standardized and automated income logic pays for itself because all parties will be working from the same base calculation rather than competing calculations for how qualifying income should be calculated.

3. Underwriting Condition Management

Lenders are executing quality control measures before an application goes through underwriter departments. This allows them to discover missing documentation, inconsistencies with income, and incomplete files earlier in the process.

4. Disclosure Timing and Compliance

Mortgage disclosures come under strict regulations. The TRID timetable is not adjustable for reasons such as a busy processing queue. It will cause considerable risk due to missed timelines, which will create problems with the customer experience of your borrower.

Manual disclosure processes fail for three main reasons:

- Timing rules (3-day, 7-day rules, tolerances)

- Change-of-circumstance redisclosures

- Loan estimate vs closing disclosure rules

- System timestamp and audit trail requirements

- Automation helps, but it does NOT simplify compliance into a single gating step.

Automation helps, but it does NOT simplify compliance into a single gating step. Many lenders also rely on disclosure management software to standardize TRID timelines, manage change-of-circumstance redisclosures, and ensure audit-ready documentation across the loan lifecycle.

5. Investor Delivery and Post-Closing

A bottleneck can occur in the entire loan process, but it doesn’t end at the closing table. After loan funding, someone needs to put together all of the documents for that loan, make sure every detail of every document meets investor guidelines, and ensure all documents are sent to the investor successfully. When a processor has to do all this manually, it can be weeks before all documents are complete and data checks are completed.

One reviewer plainly stated that doing manual processes on top of the platform makes for a “very clunky and slow” experience. This isn’t a reflection of the core engine of the software. However, it shows what happens when lenders don’t have an automated way to get from closing to shipping to investor delivery.

Lenders that have addressed this stage are using automation to validate documents and compile the investor package for delivery. Hence files going from “closed” to “delivered” no longer require manually rebuilding the stack, per each investor’s specifications, for all documents.

Capacity Planning for the 2026 Volume Shift

This projected volume is an urgent task to complete. In past cycles of the marketplace when there is a surge in business, lenders have more headcount as a way of being able to handle these large volumes of business. In today’s market environment, lenders will not be able to use the same method of scaling through more labor and will definitely look for Encompass workflow automation. Lenders who are successful in 2026 will scale up their capacity per employee, utilizing standardized workflows in Encompass.

How Do Lenders Fix Slow Encompass Workflows Problems?

Lenders of all sizes follow a similar pattern when they successfully roll out new programs:

- Automate first the routine tasks that have clear rules. Document classification, data extraction, and income calculation are among the highest-volume yet lowest-judgment tasks in the loan process. They are ideal for automation because they typically deliver a fast return on the time and resources invested.

- Build automation inside of Encompass, not around it. Automation tools that require processors to continuously switch between tabs in their web browser simply move the manual work to another place.

- Ensure that all team members use the same set of rules when they make decisions whether it is for calculating income or reviewing whether all documents are included with the loan file. So the loan files do not get moved/wrongly rejected due to avoidable circumstances.

- Use change management to remove any problems caused by automated processes. If your business does not trust the automated process, then there will be nothing to gain from it. If an employee re-calculates the income statement using a spreadsheet, your company’s ROI will be zero. Lenders can avoid this problem by establishing trust in their systems by defining clear thresholds for system confidence. Hence, only in the event of an exception being flagged by the system will an employee be able to review the exception and perform a validation function.

- In lending, there is a responsibility to provide human review of any decision made within the system due to the regulation involved with lending. Therefore, it is not acceptable for an automated process to make a decision without some type of oversight. The result of the decision has the potential to lead to a liability rather than a feature of the lending process.

- To measure success with any automation effort, use three measures: cycle time, number of conditions that must be cleared per loan, and the cost linked with processing loans. Conduct these measurements both before and after the automation to ensure that you have clearly defined ROI.

Moving Beyond Binary Rules to Agentic AI

In the past, to resolve an Encompass bottleneck meant to develop hard, “if/then” business rules. For example, if field X is empty, then Y is null. But that only works as a basic control and does not scale up to the complexity linked with large files.

Rather than simply extracting text from a PDF document, an AI agent will cross-reference multiple data points in real time and make decisions based on the business value of those data points. For example, an agent working with a bank statement may identify an unsupported deposit of over $5000 (across multiple line items), check industry guidelines or eligibility for that investor, and create an additional task for the processor before anything is sent to an underwriter.

As an example, the active agent will receive a bank statement, identify a large, undocumented deposit, review the investor guidelines linked with the loan. Then create a task for the processor to gather an explanation for the deposit. The addition of Agentic AI will change the way that the Encompass system is used from that of a passive, document storage to that of an active processor.

Disclaimer: Emerging use cases in mortgage automation ecosystems with Agentic AI

Quick Reference: Bottleneck-to-Fix Map (Encompass Workflow Automation)

| Bottleneck | Primary Cause | Automation Fix |

| Document indexing | Classification and keying of documents manually | Automated classification of documents and data extraction |

| Income calculation | Manual logic is variable | Standard automated analysis of income with automated factors |

| Underwriting conditions | Incomplete files sent to Underwriting | Manually verify quality and completeness for Pre- under |

Where to Go From Here?

Thinking about how to improve Encompass performance or how to speed up Encompass? If you look at how you manage your Encompass workflow and audit it over time, you can identify areas that are ready for improvement based on what automation can do for your organization. Then you can start to remove any Encompass workflow problems one at a time rather than doing a complete overhaul. To find out where your business is experiencing delays in processing, track the time that a file sits at each milestone this month. This activity will typically lead you to the most critical bottlenecks that need to be solved first.

Ready to eliminate Encompass bottlenecks for good? Leverage custom Encompass API development to automate manual workflows, reduce file delays, and streamline every stage of loan processing! With us, start optimizing your pipeline today and turn slow milestones into real-time progress.

Frequently Asked Questions

1. What is the biggest workflow bottleneck in Encompass?

According to most lenders, the greatest loss of productivity for processors and underwriters is due to handling borrower documentation needing to be manually reviewed repeatedly.

2. Does Encompass have built-in automation?

Yes. Encompass provides its own built-in workflow tools (i.e., triggers and business rules). In addition to this, many lenders leverage third-party automation tools to provide deeper levels of document analysis, income calculation, and compliance with disclosures than the out-of-the-box (OOTB) rules provide.

3. Is it Encompass’s fault if my loans are moving slowly?

Probably not. The majority of the slowdowns when processing loans are generally due to how the lender configured their workflow within Encompass versus what capabilities are actually built into the application itself. Even lenders who utilize the same LOS will see greatly fluctuating cycle times depending on how much manual processing is in each lender’s method.

4. What should a lender automate first?

Start with the task that is the most repetitive within your pipeline. For most, that would be document indexing. This is a task that is performed on every single loan file and will yield the highest ROI prior to moving onto other tasks such as income calculation or condition management.

5. What causes Encompass workflow bottlenecks?

Many bottlenecks occur within Encompass due to issues with tracking manual conditions, inconsistent data entry, slow document collection from third-party sources, and poorly set-up workflow configurations. In addition, other reasons for file delay include lack of task ownership and lack of automation.

6. What are the most common Encompass workflow problems?

Duplicate data entry, missing or outdated loan conditions, lack of clear processes between teams (processing, underwriting, closing), and few reliable methods for tracking loan status are common problems. Additionally, when third-party systems are not integrated, it can lead to delays in processing.

7. Why do lenders still use manual processes in Encompass?

The vast majority of lenders still use manual processes because of an existing system, unwillingness to use new systems, and a complicated customization process that will occur if they switch to automation or new systems.