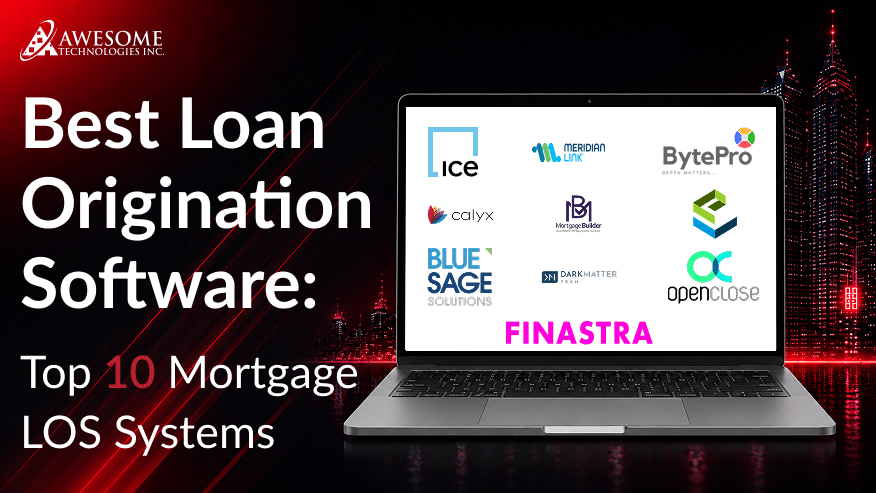

Encompass is the mortgage origination system that mid-sized and larger companies are using for their operations. It handles everything from taking the application to closing and delivery to the investors. In the last two years, it is not the system that has changed much; what has really changed is what has been running below the software itself.

At the ICE Experience 2026 convention in March, ICE announced its voice and chat AI agents for the mortgage servicing as well as a number of exception-based servicing automating agents. All this explains well that AI is no longer a simple technology but is built-in in the infrastructure of the technologies that lenders use every day. The reason why lenders are using AI is that loan processing is paperwork-intensive. Hence AI is ideal for automation. With it, it is very much possible that those who have adopted it and those who still work manually will grow bigger every quarter.

The gap in efficiency is crucial for lenders who are competing against each other since one lender can finish a loan process in two weeks and another can be stuck for the entire five-weeks. This guide explains in detail the ways AI in loan origination improves the existing workflows lenders utilize in Encompass along with the most efficient use cases. Also it discusses the relevant changes and the future of lending in terms of AI development by 2026 and later.

Therefore, whether you are an operations manager trying to assess a new AI solution or a loan officer trying to understand how the loan process has become faster today than a year ago, this guide will provide you with a brief explanation of how it actually works.

Understanding AI in Mortgage Lending

AI Applications in Mortgage Technology

AI in the mortgage lending field includes models based on machine learning, natural language, and technologies. This smart lending technology reads documents, validates information, identifies risks, and performs complex tasks that previously required humans. ICE introduces these technologies via its AIQ platform. With the use of its AI architecture called ICE Aurora, the origination process and servicing workflows will be automated. This architecture is important because AI becomes a part of the record-keeping system that lenders already rely on.

Artificial intelligence in mortgage technology does not replace the capabilities that Encompass already has to offer with its rule engine, workflow automation, and third-party integrations. It does not replace the rules that the platform comes with but instead makes those rules more powerful. Thus, it ultimately allows for the automation of repetitive activities, important insights, and data-driven suggestions

Why Are Mortgage Lenders Adopting AI Technologies?

There is a lot of paperwork in loan files. It involves the repetitive work of income and asset verification and condition clearing. This repetition is where we will see the greatest benefits from AI. A global study of mortgage lenders by IDC in 2026 showed AI as the top priority in changing the mortgage industry with lenders hoping to automate 68% of their processes within five years. AI digital transformation in the mortgage industry allows the existing teams to handle much more business without having to hire more people.

How AI is Changing Traditional Lending Processes?

Old lending processes rely more on humans to analyze the data in various documents. It also includes ensuring that the wage in a payslip matches to the one in a W-2 form. AI for mortgage lenders performs this task automatically. It means that staff will only play their part when the information doesn’t match. This change affects the nature of the job itself and leads to more use of skilled employees, making the verification process simpler and more efficient.

How AI Can Improve Encompass-Based Mortgage Workflows?

AI enables more intelligent mortgage workflows by automating repetitive tasks. Let’s explore the ways it actually does:

-

Automating Repetitive Lending Tasks

The use of AI in Encompass helps in the repetitive process of verifying the data which takes up a lot of processor time. The data depending on the document uploaded is automatically compared with the loan file without requiring manual entry at each point of the process. If you’re looking to modernize your lending operations, explore our mortgage automation software for Encompass to streamline workflows, reduce manual effort, and improve operational efficiency.

-

Improving Mortgage Data Analysis

With AI, the analysis of loan data is now possible on a scale that could not be achieved by any human team. It helps lenders find out what the bottleneck is and where the risk is more.

-

Supporting Faster Loan Processing

AI greatly shortens the time that a file stays in the processor’s line waiting for processing. Shorter processing time means less time from an application to the closing. This time frame is extremely important in a competitive mortgage environment. Most advancements are part of the bigger picture of mortgage automation in 2026. AI is a game changer in eliminating manual work and speeding up loan processing from start to finish in the lending world.

-

Mortgage Workflow Optimization

Besides automating individual tasks, AI begins to manage complex workflows in the Encompass platform. This allows moving the file from one stage to another without the human’s involvement in this process.

Organizations looking to automate file movement, notifications, and task routing can further improve efficiency through AI-powered Encompass workflow automation using webhooks.

AI Use Cases in Mortgage Lending

-

Intelligent AI Document Processing

AI can automatically identify, classify, and extract information from different types of mortgage documents. If a document is incomplete, inconsistent, or the AI is not sure about the extracted data, it can flag the file for human review. Since mortgage lenders handle documents in many formats, including scanned pay stubs, bank statements, and tax forms, automating this process can greatly reduce manual work, improve accuracy, and deliver one of the highest ROI.

-

AI-Assisted Underwriting Support

AI scans files by comparing data to source systems and highlighting differences before data arrives at the underwriter’s desk. This relieves underwriters from boring tasks while still allowing them to focus on valid underwriting cases. AI facilitates underwriting activity but doesn’t fully substitute the finding from the AUS or the underwriter’s decision. This way the underwriter is not removed from the process but instead changes the tasks he/she has to do at work.

-

Automated Data Extraction

Instead of having a human being enter the numbers from a bank statement or a pay stub, the AI does it automatically for loans. So the human errors caused by hectic time frames are vastly reduced. That level of accuracy has a great impact when you consider how many loans get processed a month, since even a minor error leads to time-consuming rework.

-

Borrower Communication Assistance

AI-assisted loan processing makes the work of loan officers easier since it helps them to answer questions from the borrowers much quicker, as well as make custom comparisons based on the latest information from Encompass. Today’s innovative solutions such as TrustEngine allow loan officers to create different presentations and send right messages to the borrowers based on the information from Encompass. Such improvement is impossible to achieve without AI since it usually requires too much time to carry out this task.

In the mortgage industry, AI can quicken the response times and provide custom comparisons for borrowers. However, it’s still important to understand the differences between AI vs. loan officer decision-making during the mortgage journey.

-

Fraud Detection and Risk Analysis

AI-based fraud detection systems can gather all fraud indicators and property data into a single workflow in Encompass. Having that data available in a single platform is not only easier but allows avoiding missing fraud alerts just because they were in a tool no one thought of looking at.

-

Predictive Analytics in Mortgages for Lending Decisions

Predictive models can tell which cases will be delayed or what applications are more likely to be completed. This allows one to direct one’s effort to the loans where some actions may actually help. This way, proactive visibility enables production managers to fix a difficult case before it starts affecting turnover figures instead of discovering this later.

Use Case Callout: Exception-Based Servicing Automation ICE launched several exception-based servicing automation agents at its 2026 conference. According to Matt Dowd, ICE’s Vice President of Product Management, the company builds AI capabilities around use cases, not as standalone products.

Generative AI in Lending: Applications in Mortgage Operations

-

AI-Powered Document Summaries

When reviewing mortgage loan files, underwriting notes, condition updates, compliance documents, etc., one may have a lot of information to go through before getting to the main stage of the process. With the help of Generative AI, it allows employees to get a logical overview of the loan without reading every document. This is particularly helpful when a loan has been transferred between employees, since the new employee can get much aware of every aspect of a loan and continue the process.

-

Mortgage Knowledge Assistants

The AI-fueled knowledge assistants get required information regarding their loans in a few simple questions in plain English. The capabilities of AI are way visible by ICE through its innovative tool, Mortgage GPT, which provides one with summaries or data in the form of graphs, charts, or additional documentation. Thanks to these tools, staff no longer need to find out through many policy documents or contact their colleagues. Moreover, this also demonstrates how generative AI is transforming mortgages through faster access to information.

-

Automated Reporting and Insights

Generative AI produces early drafts of ordinary performance reports. This helps analysts to devote their time to analysing data instead of gathering it from the ground up in every reporting period. This shift makes the role of an analyst to change from dedicating most of the week to forming the report to allocating most of the time actually using the data.

-

Employee Productivity Improvements

The workers are applying AI more and more into their existing tools to draft messages to borrowers, summarise files and produce comparisons of scenarios. Ultimately, there is no need to spend time on separate systems and manual searches that made the work complex in the past. AI tools that exist in the platform save on the efforts of a user needed to go through a standalone tool.

Benefits of AI in Mortgage Operations

-

Faster Loan Processing

Routine conditions resolve automatically rather than having to wait in the queue for a processor to get things done. It will reduce cycle time not only for a specific case but for the whole process.

-

Improved Data Accuracy

Automated extraction and verification do not get tired or lose focus like people doing manual data entry. They can catch mistakes that a human reviewer may miss after a long workday.

-

Reduced Manual Effort

Employees now do not have to perform the boring task of looking and comparing objects as their time can now be devoted to analysis and relationship with borrowers.

-

Better Borrower Experience

A quick answer from a company, fewer requests for documents, and a more individualistic approach during the loan process are due to AI. AI is basically removing obstacles that caused delays previously.

-

Improved Operational Visibility

With the help of AI-powered dashboards, executives can monitor pipeline health in real time rather than through conventional reports compiled manually from different sources.

Challenges of AI Adoption in Mortgage Technology

-

Data Privacy and Security

AI systems manage huge amounts of sensitive data, including borrowers’ Social Security numbers, income information, bank account details. Therefore lenders must secure AI systems using encryption and access control. When it comes to security risks, any AI application can pose a bigger risk for borrowers’ data.

-

Regulatory Compliance Requirements

The recent document from Fannie Mae (LL-2026-04) as well as the bulletin from Freddie Mac (Bulletin 2025-16) highlights the importance of proper governance and control, validation, and risk management while applying artificial intelligence and machine learning in mortgage lending. Hence, lenders won’t be able to consider AI-driven lending decisions as a technical matter without worrying about compliance.

-

Maintaining Human Oversight

AI automation in lending must help us in our important lending choices. However, AI can never take the role of a human being. Oversight is vital here as it ensures that exceptions are properly checked, AI-powered recommendations are justified, and we follow the requirements of the market, company policies, and business regulations. This is why it is important to maintain a proper balance between automation and human judgment.

-

Integrating AI Into Existing Workflows

A lot of lenders have legacy and customized processes within the same Encompass system, which makes the connection of AI systems and tools to these procedures a complex process. AI-powered mortgage workflows may require a lot of planning and could lead to inefficient AI integration.

The correct kind of AI implementation is crucial to successfully adapting the technology. Integration with Encompass should be smooth and work alongside existing systems, third-party software, and compliance. Read our complete guide on AI integrations for Encompass.

The Future of Artificial Intelligence in Mortgage Lending

-

AI Mortgage Copilots

We can expect that AI assistants will become integrated directly into the workflows of loan officers and processors. These advancements will extend beyond just summarizing documents. The AI mortgage Copilots will begin to help with underwriting preparation, compliance checks, and real-time borrower scenario planning. Instead of requiring the workforce to remember to use a separate tool, these assistants will offer suggestions within the existing screens that processors use daily.

-

Agentic AI Workflows

Agentic AI represents the next major step for platforms like Encompass. Instead of simply flagging issues, these systems can reason across an entire loan file and may resolve routine gaps autonomously. For example, they can request a missing document or reconcile a data discrepancy without waiting for human direction. This is the same category of technology ICE demonstrated with its exception-based servicing agents. So it’s reasonable to expect origination workflows to follow a similar path.

-

Predictive Lending Intelligence

In the coming years, lenders are beginning to adopt the use of predictive models. This will not only allow them to accurately evaluate the possible risk that comes with a specific loan. They are also able to forecast the upcoming trends within their pipeline as well as improvements needed in manpower and organizational profitability.

-

Intelligent Mortgage Operations

The large trend indicates that Encompass will be changing from a file processing system to an intelligent system which easily picks a delay in a task and helps managers understand which part of the work should be given more importance. Similar changes have already come in other industries, where software grew from a passive record-keeping system into an active decision-support tool.

-

More Personalized Borrower Experiences

AI-generated loan comparisons, annotated video explanations, and chat-based summaries are changing how loan officers communicate with clients. The fact is that borrowing services offered by lenders are becoming more and more personalized, as more and more AI tools are integrated into actual Encompass data. Due to the increasing expectations of borrowers of a personalized experience, which they get from other digital services, lenders that fail at providing it will see the negative impact on their conversion rates.

Best Practices for Adopting AI in Mortgage Workflows

- At first, it is important to define which use cases should be prioritized with the focus on problems that require the most time or may create the biggest risks rather than using AI tools just because they exist in the market. The audit will allow you to detect the location where the files actually get stuck providing a chance to indicate your starting point.

- It is essential to ensure data quality because even sophisticated AI models will return unreliable results in case of using inaccurate or incomplete loan data. Cleaning the ways of data processing may be more important than even the use of an AI model.

- It is better to focus on security and compliance from the very beginning to build governance and documentation in the process rather than having to make the process backdated after the regulatory body raises questions. Involvement of compliance specialists will save plenty of time.

- Measure AI performance continuously, tracking accuracy, exception rates, and cycle time improvements to confirm a tool is actually delivering the value it promised. A tool that looked great in a vendor demo doesn’t always perform the same way against your specific loan mix.

- Keep human decision-making involved on every high-impact file, since accountability for lending decisions remains with the lender, regardless of how much AI supports the workflow. The goal is to improve your team’s judgment, not replacing it entirely.

Wrapping Up

Artificial intelligence is transforming residential lending in amazing ways. Companies like Encompass remain in the forefront of this revolution as they are moving to smarter platforms that now offer automated verification, finding out possible risks, and fostering rapid, consistent decision-making. The banks that are achieving the best outcomes are not just the ones that aim to accept any new AI trends but rather the ones where automation, quality of data, and compliance are thought of as one single unit. As agentic AI and the technology of the existing lending systems keep advancing, the most challenging task remains evaluating AI applications for their practicality and relevance to business goals, compliance and regulations.

It is essential to undergo an evaluation right now because the difference between lenders that have put AI lending into practice and those who have not is alarming. Small lenders who have clear applications and strong governance have far better success than those automating everything at once. This technology will keep evolving into the future, and those companies that understand what is happening in this moment will be able to remain leaders in the industry for a long time. We can surely say that the future of AI in mortgage lending will be brighter with the latest technologies provided by a reliable provider such as Awesome Technologies Inc.

If you wish to upgrade your lending operations, Awesome Technologies Inc. can assist you in making the Encompass Loan Origination System more efficient through the utilization of AI-based workflow automation, process improvements, and system integrations. Working with us, you can streamline lending operations and decrease the need for manual work. Let’s connect!

Frequently Asked Questions

1. What is the role of AI in loan origination?

AI in mortgage lending uses machine learning, document recognition, and agentic automation to review, compare, validate, and extract borrower information. The goals are to support documentation, help streamline underwriting and service workflows.

2. How is AI used in mortgage workflows?

AI allows automation of routine processes such as matching documents, obtaining various pieces of information and highlighting questions that have to be checked by people.

3. Can AI improve loan processing?

AI allows for automated performance of standard operations that require no involvement of human beings. This leads to the reduction in time of processing files and makes closing faster as well.

4. What are the benefits of AI for mortgage lenders?

Faster processing of loans, more accurate data, less manual work, better communication with borrowers, and better insights into operations.

5. How does AI help mortgage underwriting?

AI assists by analyzing income, asset, and credit information, identifying inconsistencies, and preparing files for underwriter review. At the same time, it is essential to keep the underwriting decisions subject to AUS findings, investor guidelines, lender policies, and human judgment.

6. What role will generative AI play in mortgages?

Generative AI will keep expanding into document summarization, conversational data assistants, automated reporting, and drafting borrower communications, tools like ICE’s Mortgage GPT already demonstrate this direction clearly, and adoption is only likely to accelerate.

7. Is AI secure for mortgage companies?

AI is secure due to lenders utilizing encryption, access controls, and documented governance, while the sensitive data of borrowers requires security from the start.

8. What is the future of AI in mortgage lending?

Expect agentic AI to manage repetitive tasks, smarter AI copilots assisting loan officers, maintaining pipeline wide predictive insights, and regulators still pursuing explainable AI as part of their baseline requirements.