The rapid pace of business growth often comes to a halt for many mortgage companies. This is known as the growth ceiling problem. It occurs when a company cannot support an increase in volume with their existing manual process.

The loan team begins to feel overwhelmed by the increasing amounts of email, follow-up and document verification activity that happens each day. Even the smallest tasks affect the speed and efficiency of the entire process.

Many companies think that hiring additional employees will solve this problem, but it simply increases the costs and complexity of the operation without solving the underlying issue.

The real issue is the lack of scalable systems in place. As a result, there is no way to automate the processes linked with lending, nor is there any type of system that is structured to allow for rapid expansion of a lending company.

To overcome this ceiling of business, lenders must introduce mortgage business tools. Because of this, lending will become faster for the lender and scalable for both lenders and borrowers.

Digital Scalable: Understanding the Gap Most Lenders Miss

While many banks think they are growing because they’re using technology now, this doesn’t necessarily mean they are growing fast enough.

Most of these technologies operate separately from one another. Therefore, data from CRM, LOS, and communication tools don’t always transfer well.

The true divide is between using a process and creating a detailed workflow. Thus, while using separate tools can only create small gains, creating a full workflow uses all of the pieces to create larger gains such as productivity.

Without being integrated closely together, the teams/people who perform these tasks are relying on email and spreadsheets to communicate their progress.

The Invisible Friction Layer in Mortgage Operations

Invisible friction can cause mortgage operations to slow down. These are unimportant little tasks that just pile up after a while.

Things like checking loan status, sending out reminders, updating systems, and correcting minor discrepancies in data are examples of this type of activity.

However, another source of friction is switching between systems. Employees have to switch between multiple platforms to complete one task. Eventually, the increase in errors will delay decision-making.

Although invisible at times, this friction affects performance directly.

Digital mortgage software solutions help remove friction by automating routine tasks and integrating systems into one streamlined workflow.

From Tools to Systems: Rethinking Mortgage Technology Architecture

Most lenders utilize several resources but are nonetheless displeased by the productivity of those resources. This is not an issue with resources, it is related to the fact that they do not have an effective “system” in place.

A resource will provide a solution to one of the many jobs it must perform. A system will enable all jobs to connect to one another.

With a system-based solution, information flows through each step of the process. Jobs can occur automatically without any manual resources. Staff does not have to continuously follow up or change the system.

By employing a system-based approach, confusion is reduced. In addition, the predictability of daily operations will be greatly improved.

In order to experience successful value addition, lenders need to change from thinking of themselves as using resources to thinking of themselves as having an integrated system.

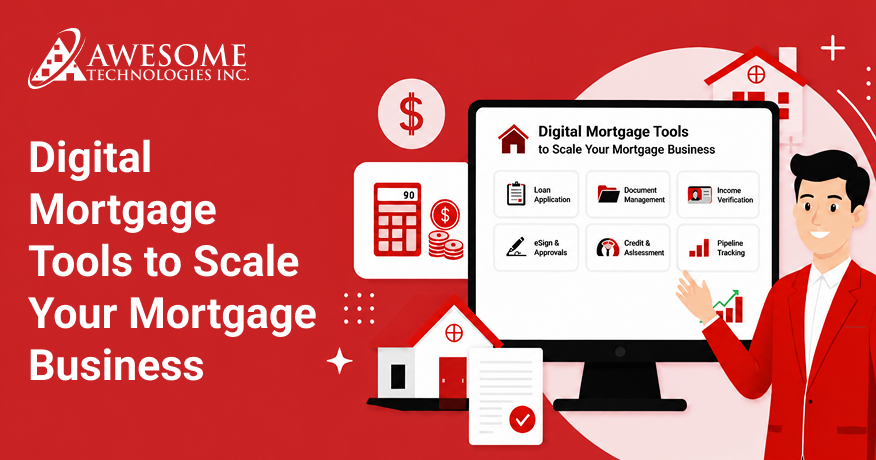

Top Digital Tools to Scale Your Mortgage Business

An efficient digital mortgage operation relies on a unified technology stack instead of separate tools.

While each of these tools performs a set function, the true efficiencies result from the ability to share data with one another through APIs, workflows and event-driven automation.

Below is a deeper technical breakdown of each core component:

1. Loan Origination System (LOS) – Core Processing Engine

The Loan Origination System (LOS) is the primary platform for processing loans in the mortgage industry. It includes processes to manage the complete loan lifecycle from application through closing.

Technical functions include:

Collecting applications and structuring data

- Creating and tracking loan files

- Routing underwriting workflows

- Tracking and resolving conditions

- Integrating with credit bureaus, pricing engines and investors

The LOS serves as the System of Record for executing loans. So, it provides an extensive audit trail to ensure all actions of the system are recorded and time-stamped.

2. CRM (Customer Relationship Management) – Borrower Data & Engagement Layer

The CRM software handles everything that relates to a borrower and their loan, from beginning to end.

Technical functions include:

- Capture leads that come in through online forms, advertisement, or from your partners

- Mark the lead’s progression through the pipeline (lead → application → closed loan)

- Automate communications to borrowers (email, text, reminders)

- Maintain up-to-date borrower profiles

- Log borrower activity every time there is contact with them

Most modern mortgage CRM tools also integrate with an LOS system via APIs to have real-time verification of borrower-to-loan relationships.

3. Automation Tools – Workflow Execution Layer

The automation tools will allow you to perform rule-based execution on any task without needing human input, such as:

Technical capabilities include:

- Using triggers to start workflows for automated responses (if X occurs then Y action happens)

- Automating the assignments of tasks to staff

- Automating system-wide updates of the status of any given loan

- Creating triggers for requesting documents from a borrower

- Creating SLA reminders and escalations for a borrower

4. Document Management Systems (DMS) – Secure Data Repository

Document Management Systems keep track of documents and allow people to manage documents safely.

Technical functions include:

Key technical features include:

- Encryption (data at rest and in transit).

- Optical Character Recognition (OCR) to extract information from images.

- Maintaining the version on an updated document.

- Role-based access controls (RBAC) on documents.

- Automated tagging and indexing of documents.

When you integrate with your LOS and CRM, you will automatically have documents linked to a borrower’s file.

5. Compliance Tools – Risk & Regulatory Engine

Compliance services ensure that all loans originate following regulatory requirements, including TRID (TILA RESPA Integrated Disclosure), RESPA (Real Estate Settlement Procedures Act), and Fair Lending Guidelines.

Technical functions include:

- The user can expect the following compliance functions:

- Automated rule validation engines to check compliance with the rules.

- Audit trails generated by immutable log files.

- Real-time compliance checks while processing the loan.

- Risk scoring models to assess risk during the loan’s origination process.

- Exception flags and alerts.

Compliance tools provide a continuous monitoring layer throughout the loan lifecycle.

6. Analytics & Reporting Tools – Decision Intelligence Layer

Analytics tools convert the raw data generated by mortgages into actionable insights so the user can benefit from this insight to make better decisions.

Technical functions include:

- Real-time dashboards (showing the current pipeline, conversion ratio, and cycle time).

- Key Performance Indicators (KPIs) to track cost per loan, fall-out ratios, and productivity.

- Predictive analytics to forecast the amount of loans you can expect in the future.

- Data warehouse and data aggregation.

- Automated executive reporting.

Analytics tools will usually gather data from your LOS, CRM, and automation into one central warehouse.

Read also -> Top 10 Business Intelligence (BI) tools 2026

How Integration Connects Everything (Critical Layer)

An integrated architecture will facilitate data transfer via:

- API’s (Application Programming Interface)

- Webhook (real-time event triggers)

- Data pipeline (batch + streaming sync)

Example of a Connected Workflow

When a borrower submits an application through the CRM system:

- CRM automatically transfers data through API to LOS.

- LOS automatically creates a loan file.

- Automation tool creates document requests.

- DMS uploads and links documents.

- The compliance system runs a rule set in real-time.

- Analytics dashboard updates in real-time.

Business Impact of a Connected Stack

A connected stack has a positive impact on businesses due to the following reasons:

- Loans are processed much faster

- Data is more accurate across multiple systems

- Leadership can see a real-time view of their operations

- Borrowers have a better experience and fewer delays when closing their loans

Choosing the Right Mortgage Tool for Business Intelligence

| Factor | What To Look For | Why Does It Matter? |

|---|---|---|

| Ease of Use | Easy-to-use designs with dashboards that are easy to understand | Will save your time and reduce the amount of confusion |

| Real-Time Data | Will update your data in real time | Will help you make quick business decisions |

| Integration | Connects with your Loan Origination Systems (LOS) and Customer Relationship Management (CRM) systems | Keeps all of your data in a single location |

| Reporting | Providing you with clear and concise reporting | Easily track your performance |

| Scalability | Growing with your business | Allowing for future opportunities |

| Insights | Show you trends and assess issues | Helps improve business decisions |

| Efficiency | Assist in making better decisions for your business | Less manual work allows you to accomplish more work faster and reduce mistakes |

2026 Industry Insight

By shifting to the development of fully integrated digital mortgage ecosystems, lenders will have greater scalability than ever before. It is due to the fact that lenders now use system-first architecture and data-driven workflows.

Because of the digital mortgage tools for lenders, lenders are able to process more loans with fewer operational resources while still remaining compliant and consistent.

Automation as Infrastructure, Not a Feature

Consistency and speed are essential in modern lending operations. Automation in mortgage allows for the management of tedious tasks such as getting reminders, writing status updates, requesting documents and tracking.

Lenders that think of automation as infrastructure build much more stable and scalable operations than lenders who view efficiency as an additional feature.

Integration Before Innovation: Why Connectivity Drives Everything?

When it comes to adding new tools for lenders, integration needs to be their first focus. Without this, there will be no integration between the lenders’ systems and this will lead to disconnected, non-efficient systems.

Integration allows different platforms to communicate with each other in real time by sharing data. Additionally, integration enhances speed in all updates that are automatically sent between all of the systems.

To build tools that truly fit your workflow, consider investing in mortgage software development services that align with your business goals.

The Borrower Journey Reimagined Through Digital Systems

The implementation of digital mortgage tools leads to improved borrower experiences. It allows users to complete online applications and submit their documents while receiving live updates about their loan progress.

Lenders achieve workload reduction through digital mortgage tools which enable them to handle increased borrower volumes while maintaining service quality.

The “Invisible Work” Elimination Model: Where Efficiency Actually Comes From

The mortgage industry can be broken down into the following “hidden” work: follow-ups, reminders, updates, and coordination.

These activities may require high amounts of time but do not directly contribute value to customers.

Another example is checking the status of a loan via a dashboard rather than calling a lender to check on each application or reporting.

By removing hidden work from the mortgage loan processing process, mortgage teams save time and become less stressed.

The true measure of efficiency in the mortgage industry is not just speeding up existing processes but also eliminating unnecessary processes.

Explore our Business Intelligence dashboard to get clear, real-time insights that help you make smarter mortgage decisions faster.

Data Discipline: The Backbone of Scalable Mortgage Operations

The ability to have well-disciplined data can result in creating accurate, consistent, and structured data.

When data is organized, lenders can use it to create more reliable reports and develop better decisions. It also supports compliance needs, as when lenders have accurate data, they are able to maintain accuracy in reporting to their regulators.

Digital mortgage tools for lenders facilitate the maintenance of accurate and consistent mortgage data through the use of standardized data inputs.

Lenders who practice data discipline build a strong base upon which to expand their operations.

Real-World Use Cases: How Digital Tools Transform Daily Lending Workflows?

Lenders are going through a remarkable transformation by utilizing integrated LOS and CRM systems like the Encompass Ecosystem from ICE Mortgage Technology.

For example, a U.S. lender implemented a fully integrated workflow between their CRM and Encompass whereby the process for updating loan information with Borrower’s data was automated.

Previously, loan officers had to manually re-enter Borrower’s information from the CRM into the LOS.

Another lender reported faster document collection cycles due to the automated reminder system built into the Encompass LOS.

Instead, audit trails and automatically validate rules provided by Encompass workflows also assist compliance teams.

This helps lenders discover when disclosures are missing much earlier in the process than they would discover through traditional post-review auditing.

The ROI Curve of Digital Mortgage Tools: When Value Becomes Visible

In terms of the ROI of Digital Mortgage Tools, it typically grows over time after being implemented and utilized.

A company’s initial costs associated with the use of Digital Mortgage Tools will occur in “startup” mode before actually being productive (usage).

Therefore, it is important for lenders to understand that the ROI generated by mortgage business tools is neither quick nor one-time, but rather compounded over time through the continuous use of these tools.

Scaling Without Hiring: The New Mortgage Operating Model

No longer is it necessary for lenders to add significant numbers of staff to support a growing volume of loans being processed.

Instead, lenders can use digital tools to provide the same service and/or process a greater number of loans with less staff.

In practice, lenders can create a more viable and sustainable model for growth through cost reductions and improved consistency.

Same Tools, Different Outcomes: Why Execution Defines Success?

It’s important to understand that even the best tools will not produce a successful execution unless they have been set up with good workflows, process controls, and proper training for everyone who uses the tool.

A well-defined process is as important as having a good tool. If you execute your process poorly, you can still be inefficient with very good tools.

Success is really tied not only to your use of technology but how effectively you utilize that technology.

Risk, Compliance, and Control in a Digital-First Environment

Managing risk and compliance in a digital-first mortgage world is done through automated processes and system controls.

Today’s technology provides multiple points throughout the loan transaction to enact automated compliance checks and mitigate the chances for human error.

It is done by providing a set of built-in rules to follow, including regulatory compliance for requirements, such as: loan disclosure, eligibility, and documentation.

Finally, with the use of automated audit trails, which track each transaction as it is recorded in the system, organizations will have an ongoing record of their actions in near real-time.

This creates greater transparency for all parties (lender, borrower, regulatory agency) creating a stronger risk and compliance environment for the lender and faster processing times for loans.

Future-Proofing Your Lending Business: Digital Strategy for 2026 and Beyond

Artificial intelligence, automation, and interconnected digital ecosystems will shape the future of lending. With AI, lenders can analyze data and determine risk levels and creditworthiness using a variety of criteria that are not typically considered by humans.

Automating repetitive activities such as gathering documentation, updating the status of a loan application, and routing workflows allows employees to spend less time performing these functions.

By utilizing these technologies as early adopters, lenders will be able to earn competitive advantages in speed, accuracy, and efficiency.

Final Insight: Scaling Mortgage Operations Is a System Design Challenge

Building a mortgage company’s scale is not about more effort or longer working hours. It is about creating and implementing systems that can support enterprise-level growth with minimal disruption to operations.

Technology-based mortgage software solutions enable lenders to create more efficient, streamlined, and interconnected workflows.

When designed properly from the beginning, loan processing workflow systems enable all loan processing stages to become more predictable and efficient.

The methodical approach to mortgage company organization enables lenders to experience fewer process interruptions, reduced error rates, and enhanced borrower satisfaction.

Lenders who invest in superior workflow designs will lead the industry in 2026 and beyond.

Are you ready to scale your company more intelligently? Discover how our mortgage business intelligence tool can revolutionize your company’s productivity and effectiveness.

FAQs

1. What are digital mortgage tools?

Digital mortgage tools are software and technology solutions that help lenders manage, automate, and streamline the entire loan process — from application to closing. They replace slow, paper-heavy workflows with faster digital alternatives like e-signatures, automated underwriting, and online document collection. These tools give mortgage teams real-time visibility into every loan, reduce costly errors, and help borrowers get faster approvals. In short, they make the lending process smoother for both the lender and the borrower.

2. How do digital tools help scale a mortgage business?

Digital tools support the growth of a mortgage company by decreasing the time required for manual processing, increasing efficiency and supporting higher loan volume. As a result, lenders can handle more loans, and improve the speed at which loans are closed.

3. What tools are essential for mortgage lenders?

The mortgage lending process requires lenders to use all six essential tools which include LOS, CRM, automation platforms, document management systems, compliance tools, and analytics dashboards.

- The loan processing system operates through an LOS system which directs loan management activities

- The CRM system keeps track of borrower information

- The automation systems manage operational tasks

- The document systems function as file storage systems

- Compliance tools maintain regulatory compliance and analytics systems deliver performance metrics.

4. How much ROI can lenders expect from digital tools?

Digital tools deliver lenders financial returns through three main benefits which include reduced loan costs, improved operational efficiency and augmented loan processing capacity. The ROI for the project will depend on how well the organization implements its systems and integrates its current technologies. Lenders experience their first operational benefits through gradual performance improvements.

5. When should a lender invest in digital transformation?

A lender should invest in digital transformation when manual processes start slowing down operations, causing delays, errors, or limiting loan volume.