2026 is going to be an important year for mortgage lenders. The market and how loans are being asked for will be very different and borrower expectations are at their highest level ever.

Today’s borrowers want quick and easy transactions-based on technology, not on slow-moving outdated processes. Lenders need to look at their processes, communication, and value to the customer throughout the entire loan process.

At the same time, compliance is becoming tighter and somehow difficult to achieve. It is because regulators are keeping a closer watch and also because documentation errors may lead to more costs.

The lenders who are winning today are not necessarily the largest lenders. They are the ones that have redefined their loan origination process with innovative technology, improved data quality and processes that focus on assisting borrowers comprehensively.

This guide explains how to originate loans efficiently and effectively in 2026.

From identifying and removing bottlenecks to using AI smartly, this guide should provide mortgage professionals with actionable information that can help them be successful.

What is Mortgage Loan Origination?

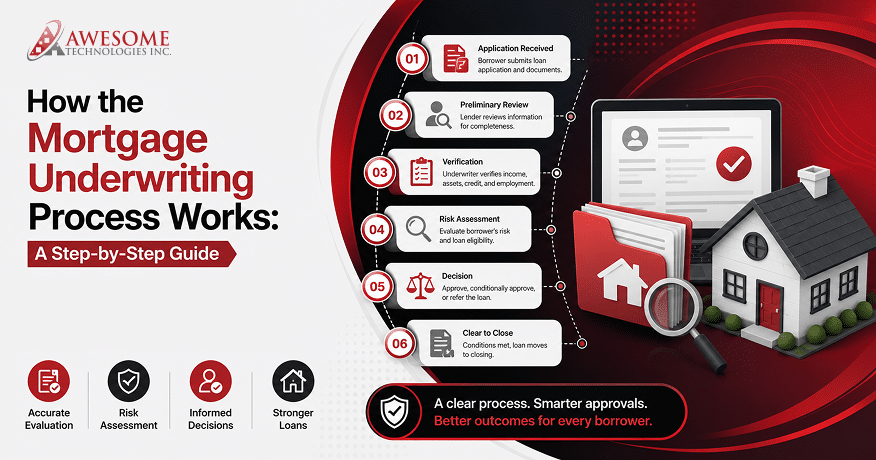

The mortgage loan origination process consists of the entire sequence of actions from when a borrower applies for a mortgage to when the borrower gets the mortgage money.

The steps of mortgage loan origination are divided into 6 stages:

- Pre-qualification

- Formal application

- Document collection

- Mortgage Underwriting

- Approval

- Closing

It is not a single step. It is a series of stages that move a borrower from “I want to buy a home” to “here are your keys.”

Each of these stages requires various participants in the process:

- A borrower provides documents proving their financial status

- The loan officer is responsible for facilitating the entire process

- An underwriter determines an applicant’s creditworthiness

Therefore, the lender is ultimately responsible for making the loan funding decision.

For lenders that have effective mortgage origination processes, they experience closures more quickly and at lower costs, as well as greater borrower satisfaction.

However, in cases where lenders have ineffective origination processes, closings will take longer to complete, risk of violating compliance increases, and revenue will hence decline.

How Mortgage Loan Origination Has Evolved in 2026?

Recent history has seen a considerable transformation in mortgage origination, from the days of large file cabinets full of paper, tedious data entry, and multiple phone calls to locate missing paperwork, to an almost paperless and manual entry-free digital-first mortgage origination process.

Many lenders have adopted a digital-first model and now take applications, verify documents and provide real-time updates as soon as the borrower hits “submit.”

The introduction of AI and predictive analytics has further changed the entire ecosystem of mortgage origination, marking a shift towards mortgage digital transformation.

The use of analytics helps lenders to define borrower risk, identify potential challenges, and help in making pricing decisions.

Borrowers’ expectations have changed, too. They compare their mortgage experiences to booking flights, and managing their bank accounts. It is evident that they want personalization rather than generic loan products which become bothersome for them.

Common Challenges in Mortgage Origination

Although improved technology is available today, many lenders face difficulties such as:

- Manual bottlenecks can significantly impair the efficiency of the loan pipeline.

- Constant compliance and regulatory requirements add an extensive amount of pressure to loan officers.

- Loan officers’ ability to consistently complete TRID and RESPA guidelines at every stage continues to be a challenge.

- Loan officers are frequently challenged to coordinate verification processes and systems.

- The length of the loan application process may result in borrowers giving up on their application.

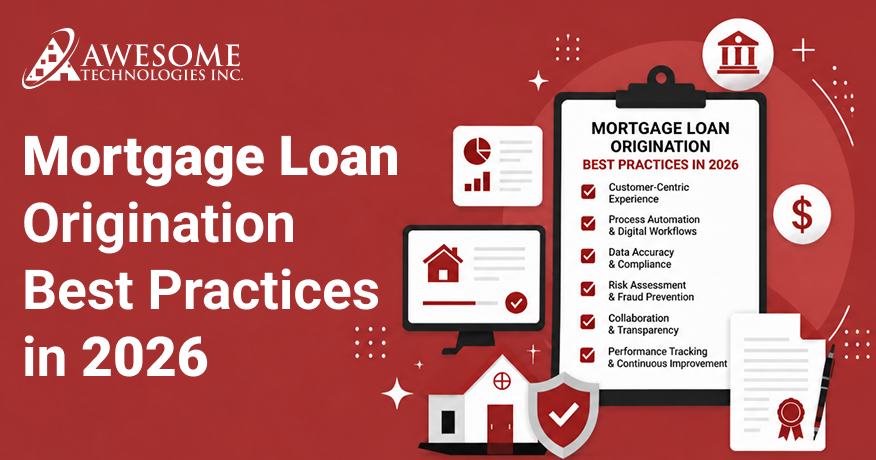

Best Practices for Mortgage Loan Origination in 2026

Achieving the right outcome by origination standards should not involve trying all of the new origination technology out there in the market.

More focus should be placed on creating a process that will be standard and consistently executed, offer a borrower friendly experience, and will be scalable.

Let’s explore the best practices of loan origination in 2026:

- Automate Routine Workflows

With minimal manual input, many day-to-day tasks can be automated such as document collection, data entry, responding to the status of the loan file, and sending reminders to borrowers to get needed documentation.

While manual handling increases the risks of errors, AI helps in improving efficiency and consistency across the entire loan process.

On the other hand, when AI is used to perform these tasks, loan officers can focus on: managing complex borrower situations, building relationships and handling deals smartly.

Fraud detection tools that use automation to find fraudulent applications are constantly running in the background of all applications. These tools flag inconsistencies in applications immediately and at scale. This is difficult via manual reviews.

- Adopt a Scalable, Cloud-Based LOS

The LOS (loan origination system) should be more than just storing loan files. It should automate workflows related to processing a loan file.

Additionally, it should provide functionality to recognize likely compliance problems, can integrate successfully with third party systems and provide real time visibility of loan processes.

When looking for a new LOS, evaluate the LOS for the following:

- Built-in compliance management functionality

- Robust integration capabilities

- Ease of use

- Strengthen Underwriting with Data-Driven Decisioning

Underwriting is the area in which a loan transaction can be won or lost.

Whether it is calculating Debt-to-Income ratio incorrectly or missing out on job verification documentation, such factors disturb loan processing.

Risk modelling with AI provides consistency to the underwriting process by analyzing borrower data more quickly and with greater accuracy. With the use of risk modelling that uses AI, this can be removed since each borrower is evaluated using the same criteria, at all times.

- Prioritize Compliance at Every Stage

Compliance should never be an afterthought. With regulations such as TRID, RESPA, and CFPB, every step in the loan transaction process must include verified documentation.

Automated disclosures and audit trails resulting from automated processes decrease the manual labor involved in managing compliance and reduce the chances of errors.

However, there are always deviations to every rule. So, what was compliant a year ago may not still be compliant today. Therefore, it is very important to remain aware of the current day compliance issues and solve them as they come.

- Personalize the Borrower Experience

Every borrower wants to have a personalized experience. This means providing them various options that meet their needs, setting timelines as per the borrower’s situations, and providing on-time coordination.

This can be done by:

- Using borrowers’ data to provide them with loan product suggestions right away

- Proactively updating them with milestone alerts

- Establishing a self-service portal for borrowers so they can upload documents and check the status of their loans.

- Integrate Systems Seamlessly

If your LOS and other important systems do not connect with CRM, Credit, Appraisal Vendors or Title Partners seamlessly, it will ultimately lead to errors and/or delays.

On the other hand, strong integration results in:

- Data automatically flowing between the systems

- Less manual work and more efficiency

- Fewer delays in the process

- The better chance of the deal moving through the entire process (Application through to Closing) efficiently

- Leverage Predictive Analytics

Predictive analytics provides lenders with great opportunities to do business.

By using predictive analytics:

- Lenders can proactively identify borrowers likely to refinance or show early signs of risk

- Identify early signs of financial difficulties

- Recognize areas in which they may find equity.

Lenders can therefore reach out to the borrower when it is time for them, and not wait for the borrower to contact them.

- Educate and Empower Borrowers

When you educate your borrower with clear onboarding emails, short “explain” videos, and personalized consults, the borrower can move faster and with more confidence through the loan origination process.

This will help to decrease the number of borrowers who drop during the process and expedite the time to close the loans.

- Monitor Portfolio Performance in Real Time

Continuously monitor borrower behaviour post-origination to identify early signs of distress, so lenders can act proactively before issues arise.

This ultimately reduces risk and increases the overall health of a lender’s portfolio and its performance.

- Build a Technology Stack, Not a Single Tool

Great lenders use a combination of various software platforms/tools to help run their lender businesses.

An example of this would be to have a fully AI driven underwriting software work with your current CRM system together as a single entity to get the best results possible.

The Role of AI and Technology in Mortgage Origination

The previous concept of AI being just a tool for the future in mortgage lending is no longer true.

Today, AI plays a role across multiple stages of the origination process, including:

- AI has the ability to extract and validate information about borrowers from documents within minutes.

- AI fraud detection will analyze the patterns used to apply and flag any inconsistencies that human reviewers may not easily catch.

- AI also employs real-time market data to provide lenders with a more accurate loan pricing decision within a much quicker time frame than ever before.

- The methodologies used for evaluating credit risk have also evolved to include machine learning models that assess a larger data set.

- Fraud detection is one of the most valuable AI applications for mortgage origination. The effectiveness of machine learning models continues to improve, as their algorithms learn from newer fraud patterns.

There are several platforms obtaining these results through predictive analytics.

- Propair.ai optimizes mortgage underwriting process and secondary market execution

- Blend creates a streamlined digital application and closing process

- Zest AI introduces consistency and fairness to the credit decision process by using machine learning

Compliance and Regulatory Considerations in 2026

Mortgage lenders have always been under the pressure of compliance.

In 2026, compliance is only more complicated than it was before and the cost of getting it wrong is the highest that it has ever been.

All lenders who are currently doing business need to know as well as possible the main regulatory frameworks related to origination.

The following Regulatory Frameworks govern lending:

- TRID regulates the timing and delivery of loan estimates and Closing Disclosures.

- RESPA deals with the relationships and fees for settlement services.

- The CFPB regulates everything from fair lending to how lenders communicate with borrowers.

These frameworks and regulations are not optional and form the basis of a legally compliant LOS system.

Automation can help to reduce the amount of human error. It also reduces the risk of failure to comply with the above regulations.

However, new technology (AI) brings about additional compliance concerns. Lenders can develop models for credit decisioning.

The CFPB is currently issuing guidance on how machine learning can be used in lending and it becomes very important for lenders to stay up to date on this new guidance.

Compliance with your lending practices in 2026 will not only be a matter of your current rules and regulations but also a matter of forecasting where future regulations may be headed.

How to Choose the Right Loan Origination System in 2026

Here is how to approach the process of selecting a new LOS.

- First understand what problem is impacting your operations the most. Is it slow processing? Compliance gaps? Poor communication with borrowers?

- Next, consider these must-have features to be in the LOS you will select: loan origination workflow automation, built-in compliance, scalability, and easy integration.

- Before you commit to any vendor, make sure you ask the following questions: how long will it take to implement the system? What kind of ongoing support will I receive? How does the LOS manage updates to comply with regulatory requirements? In addition to the subscription pricing for the LOS, what will the total cost be?

- Small lenders need simplicity, affordability and fast implementation.

- Enterprise teams need configuration, advanced reporting capabilities and support for multiple channels or ways that people will apply for a loan.

Many lenders are looking to improve the way they do business through upgrading their mortgage systems. To choose a system that will allow them to automate processes, remain compliant, and create a scalable network of systems, lenders should evaluate the best mortgage loan origination systems available.

Key Metrics to Track in Loan Origination

- The average time it takes to complete a loan is referred to as the Time to Close. If the Time to Close is too long, it means there is an issue somewhere in your workflow and should be corrected.

- The Application to Approval Rate tells you the percentage of applications that ultimately become loans. A low Application to Approval Rate indicates either a weak qualification process for the borrower or inadequacies in the mortgage underwriting process.

- The Borrower Drop-Off Rate reports how many borrowers discontinue the application process prior to an approval. If the drop-off rate is too high, this indicates that the application process is either too lengthy, too cumbersome, or a combination of both.

- The Cost Per Loan Originated determines the exact cost associated with processing, closing, and recording a loan. The lower the cost per loan originated, the greater the overall profitability of your operation.

- The Compliance Error Rate measures how often your business’s processes produce errors in documentation such as for disclosures, etc. Although a small number of compliance errors can lead to potential exposure to lawsuits or regulatory actions, the volume of both can affect your overall profitability.

- The Customer Satisfaction Score (CSAT) is a measure of how borrowers perceive their overall experience with your company in today’s competitive environment. A bad experience means fewer referrals and a loss of repeat business.

Future of Mortgage Loan Origination Beyond 2026

Generative artificial intelligence provides assistance to loan officers in preparing communications, summarizing borrower profiles, and raising flags on possible risks instantly.

Hyper-personalization personalizes the entire origination process for all their customers. It uses financial history, life stage signals, real-time behavior data, and AI-driven insights.

Lenders that establish a foundation of ethical and explainable AI practices now will put themselves in an advantageous position.

Conclusion

In the year 2026, Mortgage Loan Origination will be a function of 3 primary factors: an appropriate technology stack, sound compliance practices and a process focused on the borrower.

There is no single solution or tool that will solve every problem occurring with the origination of a mortgage.

The lenders that are performing at the highest level now have built and are using connected technology stacks; have trained and prepared their teams; and consistently measure the data elements that matter the most.

So, take a hard look at your impact points for mortgage digital transformation. Start working on those issues first and then build your future from there.

Having connectivity gaps is an obstacle for the majority lenders today. With the help of our Loan Origination System Integration Services, lenders can create an end-to-end connected, scalable origination infrastructure.

FAQs

1. What is the mortgage loan origination process step by step?

A mortgage loan must go through six steps to be originated: pre-qualify, apply formally, collect documents, underwrite, obtain approval and close on the loan.

2. What is the biggest challenge in mortgage loan origination in 2026?

The biggest challenge in mortgage loan origination is the use of manual processes. When document collection, data entry and compliance checks are all done manually, it creates bottlenecks.

3. What is the difference between a LOS and a CRM in mortgage lending?

A CRM handles leads and client relationships (so it gathers leads like potential customers and helps with communication afterwards), while an LOS is responsible for managing the actual loan process itself.

4. How long does mortgage loan origination take in 2026?

As a result of automation and new AI workflows, a lot of lenders are completing loans within a 15-25 day time frame. However, it still depends on loan complexity and borrower’s readiness.